我看到這篇文章 [1] 說, 老巴希望他的繼承人用 90/10 的比重, 投資於 S&P500 和短期國債. 不過本文的作者 Tony Dong 把主菜和配菜都代換成不同版本, 然後得出不同的結論.

原本配方的主菜 (S&P 500 股票):

- Vanguard S&P 500 ETF (VOO): 0.03% expense ratio.

- iShares Core S&P 500 ETF (IVV): 0.03 expense ratio.

換成美股全市場股票:

- Vanguard Total Stock Market ETF (VTI): 0.03% expense ratio.

- iShares Core S&P Total U.S. Stock Market ETF (ITOT): 0.03% expense

配菜 (短期債券):

- Vanguard Short-Term Treasury ETF (VGSH): 0.04% expense ratio.

- iShares 1-3 Year Treasury Bond ETF (SHY): 0.15% expense ratio.

換成長債:

- Vanguard Long-Term Treasury ETF (VGLT): 0.04% expense ratio.

- iShares 20+ Year Treasury Bond ETF (TLT): 0.15% expense ratio.

結論是: “Modifying Warren Buffett’s 90/10 portfolio using long-term Treasurys and the total U.S. stock market historically improved performance, with a better risk-adjusted return. “. S&P500 和短債表現不如美股全市場和長債 (回測期間: 197 7~ 2022). 那老巴錯了嗎?

基本上, 這篇文章寫於 2022 年六月, 而升息對債券和股市的影響主要反映在 2022 的下半年. 上半年笑得出來, 也不一定能笑到年底. 所以呢, 我還是先自己研究一下美國公債中短債、中債、長債的表現如何?

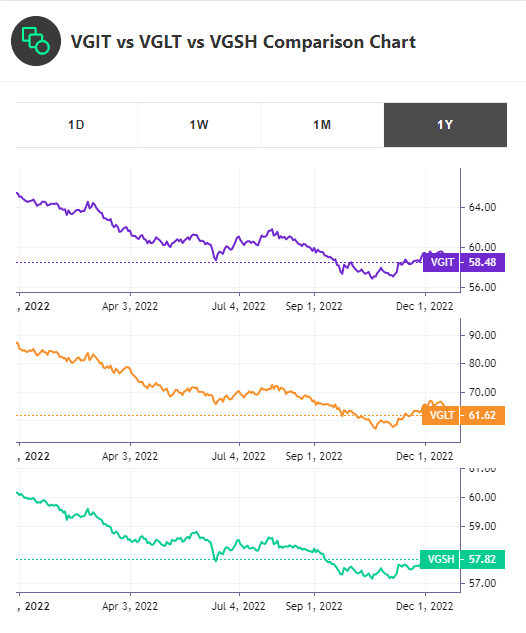

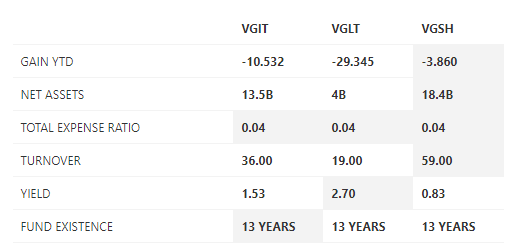

先偷瞄過, VGSH (短期國債) 和 SHY 的波形幾乎一模一樣, VGLT (長期國債) 和 TLT 也是一個樣. 所以三組各派一名代表來 PK 就行了. 借用 [2] 這個網站, 我們得到下圖:

基本上長債 (VGLT) 波形還比較平滑, 問題出在它 “一屍到底", 文章 [1] 的結論, “Modifying Warren Buffett’s 90/10 portfolio using long-term Treasurys and the total U.S. stock market historically improved performance, with a better risk-adjusted return. “, 看來還是有待商榷. 網站 [2] 還提供了下表:

所以呢? 要求穩必須選短債 (VGSH), 報酬高選長債 (VGLT), 折衷就選中期債券. 知名的綠角大大有非常多篇討論股債平衡的文章, 更是每年算一次股債配置如何勝過純股票投資. 它所選用的債券就是美債 iShare 3-7 Year Treasure bond ETF (IEI) 和 SPDR Barclays Internation Treasure ETF (BWX) 各半. iShare IEI 就等於 Vanguard VGIT, 屬於中期. 後者是世界各國政府公債的 ETF.

再加一位大師來鬥陣的話, 闕又上大師在"你沒有學到的巴菲特" 中推薦投短期公債或 7~10 年公債指數基金, 並且說長期公債價格太敏感, 波動比股票還劇烈. (1946~1981, 利率由 2.03% 升到 16%; 債券跌掉 83%). 所以他不忌短中期, 唯獨不好長期.

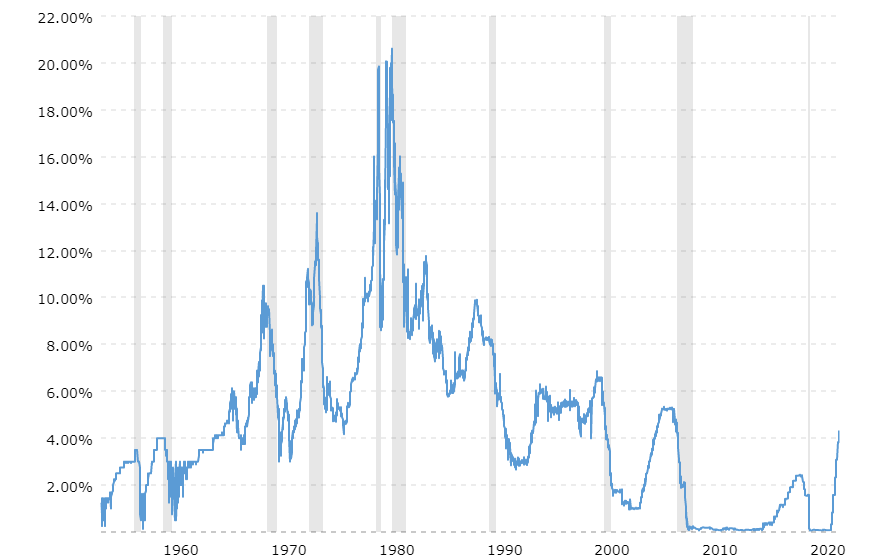

所以看著看著, 短債是否又比較有道理了? 然而, 大家覺得美國的公債利率會再次上升到 16% 嗎? 如果利率這麼高, 應該會造成巨大的貧富差距. 億萬富翁年收千萬利息; 本來就勉強度日的人, 連正常地借個創業貸款都搞得像跟欠地下錢莊錢一樣. 1981 年高利率其實是為了讓經濟衰退並降溫, 以降低通膨, 當時的通膨率高達 14.6% [3]. 只要通膨率不上雙位數, 利率也不太可能再重返兩位數字.

下圖顯示, 所以 80 年代利率頂多是 10%, 90 年代以後都不曾再見到 6.5% 之類的高利率 [4].

而且呢, 論調升幅度. 2022 年往前看一甲子都沒這麼狠過, annual change rate 達到 6085.71% [4]. 會不會反而凸顯出長債的跌幅已經反映得差不多了? 既然利空出盡, 買長債是否又是最正確的呢?

| Federal Funds Rate – Historical Annual Yield Data | ||||||

|---|---|---|---|---|---|---|

| Year | Average Yield | Year Open | Year High | Year Low | Year Close | Annual % Change |

| 2022 | 1.67% | 0.08% | 4.33% | 0.08% | 4.33% | 6085.71% |

| 2021 | 0.08% | 0.09% | 0.10% | 0.05% | 0.07% | -22.22% |

| 2020 | 0.36% | 1.55% | 1.60% | 0.04% | 0.09% | -94.19% |

| 2019 | 2.16% | 2.40% | 2.45% | 1.55% | 1.55% | -35.42% |

| 2018 | 1.79% | 1.42% | 2.40% | 1.34% | 2.40% | 80.45% |

| 2017 | 1.00% | 0.55% | 1.42% | 0.55% | 1.33% | 141.82% |

| 2016 | 0.39% | 0.20% | 0.66% | 0.20% | 0.55% | 175.00% |

| 2015 | 0.13% | 0.06% | 0.37% | 0.06% | 0.20% | 233.33% |

| 2014 | 0.09% | 0.07% | 0.13% | 0.06% | 0.06% | -14.29% |

| 2013 | 0.11% | 0.09% | 0.17% | 0.06% | 0.07% | -22.22% |

| 2012 | 0.14% | 0.04% | 0.19% | 0.04% | 0.09% | 125.00% |

| 2011 | 0.10% | 0.13% | 0.19% | 0.04% | 0.04% | -69.23% |

| 2010 | 0.18% | 0.05% | 0.22% | 0.05% | 0.13% | 160.00% |

| 2009 | 0.16% | 0.14% | 0.25% | 0.05% | 0.05% | -64.29% |

| 2008 | 1.92% | 3.06% | 4.27% | 0.09% | 0.14% | -95.42% |

| 2007 | 5.02% | 5.17% | 5.41% | 3.06% | 3.06% | -40.81% |

| 2006 | 4.97% | 4.09% | 5.34% | 4.09% | 5.17% | 26.41% |

| 2005 | 3.22% | 1.97% | 4.30% | 1.97% | 4.09% | 107.61% |

| 2004 | 1.35% | 0.94% | 2.34% | 0.92% | 1.97% | 109.57% |

| 2003 | 1.13% | 1.16% | 1.45% | 0.86% | 0.94% | -18.97% |

| 2002 | 1.67% | 1.52% | 1.92% | 1.15% | 1.16% | -23.68% |

| 2001 | 3.88% | 5.41% | 6.67% | 1.19% | 1.52% | -71.90% |

| 2000 | 6.24% | 3.99% | 7.03% | 3.99% | 5.41% | 35.59% |

| 1999 | 4.97% | 4.07% | 5.76% | 3.99% | 3.99% | -1.97% |

| 1998 | 5.35% | 5.84% | 7.06% | 4.07% | 4.07% | -30.31% |

| 1997 | 5.46% | 6.26% | 7.07% | 4.63% | 5.84% | -6.71% |

| 1996 | 5.30% | 4.73% | 7.80% | 4.73% | 6.26% | 32.35% |

| 1995 | 5.83% | 4.94% | 7.41% | 4.73% | 4.73% | -4.25% |

| 1994 | 4.21% | 2.85% | 6.56% | 2.85% | 4.94% | 73.33% |

| 1993 | 3.02% | 2.66% | 3.99% | 2.66% | 2.85% | 7.14% |

| 1992 | 3.52% | 4.09% | 4.98% | 2.58% | 2.66% | -34.96% |

| 1991 | 5.69% | 5.53% | 10.39% | 4.09% | 4.09% | -26.04% |

| 1990 | 8.10% | 7.97% | 9.53% | 5.53% | 5.53% | -30.61% |

| 1989 | 9.21% | 9.04% | 10.71% | 7.97% | 7.97% | -11.84% |

| 1988 | 7.57% | 6.89% | 9.64% | 5.72% | 9.04% | 31.20% |

| 1987 | 6.66% | 14.35% | 14.35% | 5.52% | 6.89% | -51.99% |

| 1986 | 6.80% | 13.46% | 16.17% | 5.56% | 14.35% | 6.61% |

| 1985 | 8.10% | 8.74% | 13.46% | 6.73% | 13.46% | 54.00% |

| 1984 | 10.23% | 9.92% | 12.31% | 6.93% | 8.74% | -11.90% |

| 1983 | 9.09% | 11.20% | 11.20% | 8.22% | 9.92% | -11.43% |

| 1982 | 12.24% | 13.13% | 16.80% | 8.36% | 11.20% | -14.70% |

| 1981 | 16.39% | 22.00% | 22.36% | 11.83% | 13.13% | -40.32% |

| 1980 | 13.35% | 14.77% | 22.00% | 7.65% | 22.00% | 48.95% |

| 1979 | 11.20% | 10.84% | 17.60% | 8.34% | 14.77% | 36.25% |

| 1978 | 7.94% | 6.53% | 10.89% | 6.50% | 10.84% | 66.00% |

| 1977 | 5.54% | 4.17% | 7.10% | 4.07% | 6.53% | 56.59% |

| 1976 | 5.05% | 5.37% | 5.71% | 4.12% | 4.17% | -22.35% |

| 1975 | 5.82% | 3.87% | 8.55% | 2.99% | 5.37% | 38.76% |

| 1974 | 10.51% | 9.83% | 14.33% | 3.87% | 3.87% | -60.63% |

| 1973 | 8.74% | 5.50% | 13.00% | 5.25% | 9.83% | 78.73% |

| 1972 | 4.44% | 3.00% | 6.00% | 3.00% | 5.50% | 83.33% |

| 1971 | 4.67% | 3.00% | 5.75% | 2.25% | 3.00% | 0.00% |

| 1970 | 7.17% | 5.00% | 9.75% | 3.00% | 3.00% | -40.00% |

| 1969 | 8.21% | 4.00% | 10.50% | 4.00% | 5.00% | 25.00% |

| 1968 | 5.66% | 4.50% | 6.88% | 2.50% | 4.00% | -11.11% |

| 1967 | 4.22% | 5.00% | 5.75% | 2.00% | 4.50% | -10.00% |

| 1966 | 5.11% | 4.63% | 6.25% | 1.50% | 5.00% | 7.99% |

| 1965 | 4.08% | 4.00% | 4.63% | 1.00% | 4.63% | 15.75% |

| 1964 | 3.50% | 3.25% | 4.00% | 1.00% | 4.00% | 23.08% |

| 1963 | 3.18% | 3.00% | 3.50% | 0.75% | 3.25% | 8.33% |

| 1962 | 2.71% | 2.50% | 3.00% | 0.25% | 3.00% | 20.00% |

| 1961 | 1.95% | 3.00% | 3.00% | 0.13% | 2.50% | -16.67% |

| 1960 | 3.21% | 4.00% | 4.00% | 0.25% | 3.00% | -25.00% |

| 1959 | 3.31% | 2.38% | 4.00% | 1.50% | 4.00% | 68.07% |

| 1958 | 1.57% | 3.00% | 3.00% | 0.13% | 2.38% | -20.67% |

| 1957 | 3.11% | 3.00% | 3.50% | 1.00% | 3.00% | 0.00% |

| 1956 | 2.73% | 2.50% | 3.00% | 1.00% | 3.00% | 20.00% |

| 1955 | 1.79% | 1.44% | 2.50% | 0.50% | 2.50% | 73.61% |

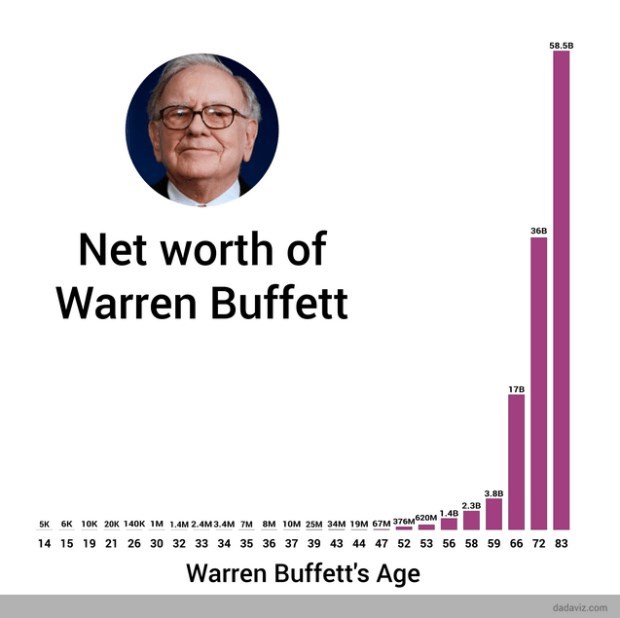

如果利率真的漲到 20%, 正常來說, 那我只好出清股票買短債吧? 但主要靠股票致富的老巴, 80 年代在做什麼? 他…他在撿便宜啊! 大家都說 “巴菲特的資產9成是50歲以後才賺到!如何讓財富像雪球,活愈久滾愈多?". 好像關鍵在於滾雪球, 人人有機會成為股神. 其實老巴生於1930年8月30日, 他五十歲的時候就是 80 年代. 當債券利率高達 20%, 誰還會跟老巴搶股票啊!? 任何神股都變得不值得一顧, 但是買了就有機會當股神!

所以逆向思考才是對的. 如果美國的殖利率就這樣飆上去, 也不要學人瘋搶債券. 還是要多買股票才能當巴菲特. 下面兩張圖都來自商周財富網 [5][6]. 80 年代如果重現, 買債券可以小富, 買對股票可以大富! 畢竟利率再高也撐不了十年, 但是好企業可以撐百年.

[REF]

- https://www.etfcentral.com/news/warren-buffett-90-10-etf-portfolio

- https://tickeron.com/pick-the-best/VGIT-or-VGLT-or-VGSH/?utm_source=Tickeron&utm_campaign=Compare&utm_content=CompareSearch

- https://www.gvm.com.tw/article/90957

- https://www.macrotrends.net/2015/fed-funds-rate-historical-chart

- https://wealth.businessweekly.com.tw/m/GArticle.aspx?id=ARTL000098348

- https://wealth.businessweekly.com.tw/m/GArticle.aspx?id=ARTL003002363